THREE SMART WAYS TO SPEND YOUR TAX RETURN IN 2022

Last year, more than 169 million people filed their taxes and received more than $365 billion in tax refunds.1 The average return was $2,815, up nearly 10% from the year before. A large tax refund can provide a chance for people to improve their financial well-being. This issue of Investment Insights discusses three of the many possible ways to spend a tax refund.

Financial Freedom

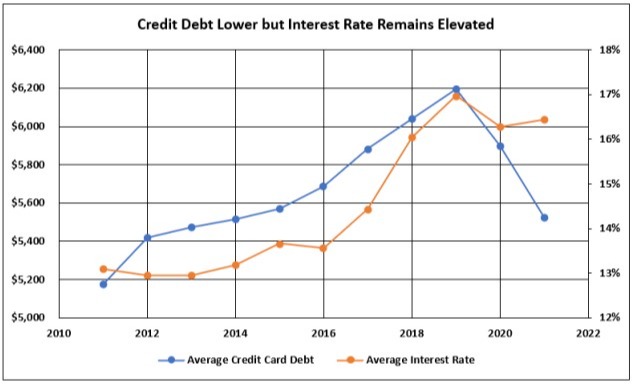

For people with high-interest credit card debt, reducing or potentially eliminating credit card debt can be one of the best uses of their tax refund. By doing so, they pay less in future finance charges. Reducing or eliminating credit card debt can be beneficial because credit card debt is often more expensive than other types of debt. In 2021, the average interest rate on credit card debt was 16.45%.2Until recently, consumer credit debt increased year over year. Between 2011 and 2019, the average credit card debt increased from %,175 to $6,194, representing almost a 20% increase. For the first time in a decade, the average credit card debt dropped to $5,897 in 2020 and dropped again to $5,525 in 2021. The likely reason for this trend is that many individuals used their economic stimulus payments to pay down their credit card debt. While the average credit card debt of the consumer has dropped, the credit card interest rate has remained relatively high. As such, the interest payments on credit cards are still comparatively large for most consumers. The following is an example using the number for average credit card debt, interest rate, and tax refund for 2021. A person with credit card debt of $5,525 with an interest rate of 16.45% is expected to pay about $900 in interest payments.3 If they instead used their entire tax refund of $2815, to reduce their credit card debt, they could save more than %460 in interest payments.4 For people with credit card debt, a smart use of a tax refund may be to reduce or eliminate high-interest debt obligations.

Financial Confidence

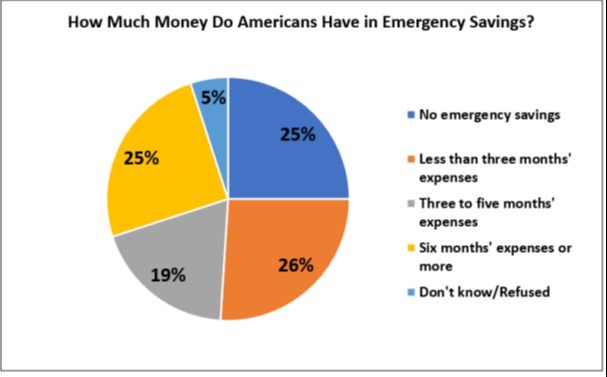

Whether to use the tax return toward paying high-interest debt or creating an emergency fund depends on the individual and their circumstances. Starting an emergency fund should be a top priority for people with no money saved up for a rainy day. An emergency fund is usually cash savings that give individuals financial confidence if something unforeseen happens, such as a job loss, medical emergency, car repairs, etc. In these instances, people without savings may have no option but to go deeper into debt, taking them further away from financial freedom. Most Americans do not have enough saved for an unexpected financial emergency. As shown in the graph below, a survey by Bankrate found that about half (51%) of Americans do not have enough saved to cover expenses for 2 months. Further, 1 in 4 responded that they have no emergency savings. In a study published in 2017, the Pew Charitable Trusts found that 56% of households experienced at least one financial shock per year.5 The Pew defined financial shock as "large unplanned expenses, such as a major home or car repair, or income lost due to unemployment, a pay cut, illness, injury, or death." The study found that the median cost of a financial shock was $2,000. One-quarter of respondents, however, faced an expense of $6,000 or more. To help soften the blow of a financial shock, consider tucking a portion of your tax refund into savings in the event of unexpected needs. If you already have an emergency fund, consider adding to it. A good rule of thumb is to have savings equal to three to six months of living expensed, depending on the stability of your income and expenses.

Financial Well-Being

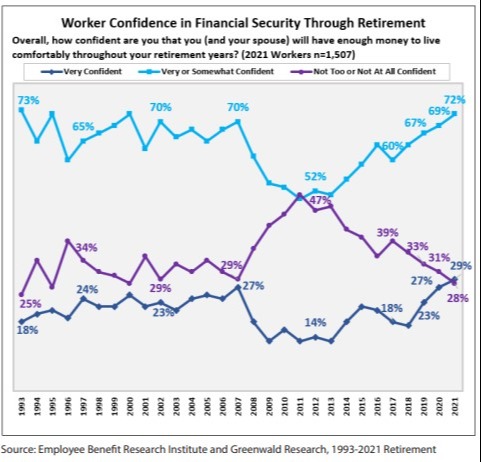

For individuals who already have an emergency fund and little to no high-interest debt, good use of a tax refund may be putting it toward retirement savings. One of many investors' biggest regrets is waiting too long and not beginning to save for retirement earlier. In face, if they could do it over again, nearly two-thirds of recent retirees would have started saving much earlier.6 Thus, these individuals may be amont the 28 of Americans who do not feel very confident about their ability to have enough money to live comfortably throughout their retirement years.7

Interestingly, most working Americans start saving for retirement later and lose the time needed for their money to grow. This is because not everyone treats this time as a valuable asset. It is an important reminder that time is an asset that loses value each day that your money is not given the opportunity to work. As the value of time is wasted, the cost of your financial goals increased, sometimes to the point that they become prohibitively expensive and unattainable. Thus, consider adding to your current savings or beginning your retirement savings journey with this year's tax refund.

Financial Plan

Ultimately, the most important part of financial well-being is having a plan. A recent survey found that 54% of Americans feel very confident about reaching their financial goals when they have a written plan vs. 18% for those without a written plan.8 Despite its benefits, the same survey found that only 33% of Americans have a written financial plan.9

This report was prepared by Khurram Naveed

Co-Portfolio Manager, LPL Operations Manager

Cornerstone Wealth Portfolios

1 Internal Revenue Service, November 3, 2021. 2 The Board of Governors of the Federal Reserve System, G-19 report.

3 16.45% of $5,525 is $908.86.

4 16.45% of $2,710 ($5,525 minus $2,815) is $445.79 which is $460.07 less than $908.86. 5 The Pew Charitable Trusts, Financial Shocks Put Retirement Security at Risk, October 25, 2017.

6 Real Deal Retirement.

7 Employee Benefit Research Institute and Greenwald Research, 2021 Retirement Confidence Survey. 8 Charles Schwab Modern Wealth Survey 2021.

9 Charles Schwab Modern Wealth Survey 2021.